Building for Both Worlds: Infrastructure for Traditional and Tokenised Finance

Stablecoins have dominated headlines in 2025, but they're just one visible piece of a larger transformation: the emergence of a tokenised financial system operating in parallel to the traditional one.This new system operates on programmable tokenised value that moves across a shared, distributed infrastructure, rather than digital value being transferred through disconnected institutional ledgers. To thrive in this evolving landscape, financial institutions must be able to build and operate products on both financial systems.

The reshuffling in financial services

Fintechs, major technology companies, and Tier 1 financial institutions are rapidly building a new tokenised financial system. Some are building the infrastructure itself, jockeying to capture transaction fees and network effects for decades to come. Others are launching products with capabilities and cost structures that were previously unattainable. The most well-capitalised players with strong market positions are pursuing both strategies at the same time.

The pace of activity intensified dramatically throughout 2025, particularly around stablecoins. Three factors converged: sustained growth in digital asset adoption globally, emerging regulatory clarity (e.g., GENIUS Act, MiCA, Hong Kong Stablecoins Bill), and a meaningful belief shift in institutions' sentiment about the long-term value of this tokenised financial system. Most recently, ten major banks, including Goldman Sachs, Citi, Barclays, and Santander, announced that they will work together to explore creating tokenised assets pegged to G7 currencies.

The financial services sector is undergoing a reshuffle. Incumbent and emerging players are both competing aggressively for payment flows, deposits, lending portfolios, and fee revenues across both the traditional and tokenised financial systems.

As customers migrate towards tokenised finance offerings, revenue and assets will follow - some financial institutions are already seeing their deposits flow out to operators in the tokenised system.

While the traditional system will coexist with the tokenised one for the foreseeable future, there is a case for the broader tokenisation of assets to disintermediate banks:

“We believe the most obvious bull case for stablecoins disintermediating banks would be much broader tokenization of the US economy. In a tokenized economy, goods and services would all be fungible across the blockchain, with one tokenized asset (e.g.,tokenized stocks, bonds, or homes) exchangeable for tokenized dollars (i.e., stablecoins). In such a world, stablecoins would become an important means of payment, resulting in a significant shift from bank deposits to stablecoins”

Goldman Sachs Research

Even without a complete disintermediation, the gradual outflow of assets and transaction volume to tokenised finance will compress the bank’s margin and undermine its competitive position.

Non-Tier 1 financial institutions are under the most pressure

Non-Tier 1 financial institutions face a particularly acute challenge. They must compete across both systems whilst operating under tighter constraints compared to their Tier 1 financial institution peers, fintechs, and major technology companies. The question for them is not whether to engage with tokenised finance, but how to do it efficiently with capital, operational and technical considerations.

They must develop the capability to access the tokenised financial system, as well as build and operate new products in a regulatory-compliant manner. Ideally, they achieve this at pace without replicating their entire technology stack and increasing their cost base dramatically.

Accessing the tokenised financial system

Financial institutions typically partner with one or more operators to build a tokenised finance proposition. Let’s take a basic stablecoin payment proposition as an example: this requires relationships with stablecoin issuers; wallet infrastructure providers for custody and transaction capabilities; and compliance tools to satisfy regulatory requirements. This partnership web grows as banks pursue more sophisticated propositions. Each partnership requires extensive due diligence, legal negotiation, and technical integration. This process can take months per vendor, fundamentally constraining how quickly banks can innovate and respond to market opportunities.

Building and operating new products

Finding the right partners solves only part of the problem. Banks must then integrate these new capabilities with their legacy systems to create functional products for their customers.

When the bank and its customers hold both traditional and tokenised assets and liabilities, the bank requires a unified, real-time view of those positions for credit decisions, analytics, regulatory reporting, customer service, and more. This demands continuous reconciliation between traditional ledgers and on-chain states.

Importantly, banks must also maintain product and payment logic that spans both traditional and tokenised financial systems.

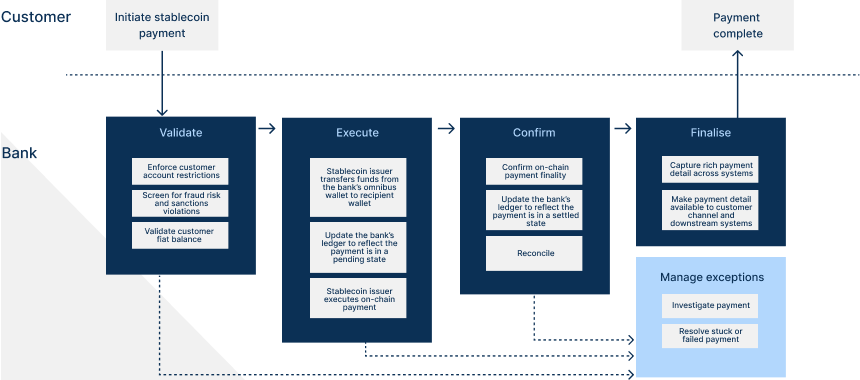

Consider a corporate customer making a cross-border payment using stablecoin. On the surface, the bank needs to convert the customer's fiat deposit into stablecoin and execute the on-chain transfer to the recipient. But underneath the surface, the bank needs to implement a rich set of logic that intelligently processes the transaction through near-real-time interactions with the core banking system, stablecoin issuer, wallet, fraud and compliance system, and the blockchain network. In addition, the bank needs to ensure a coherent and ideally consistent transaction experience for the customer, as well as a detailed audit log for downstream reporting.

Legacy systems are fundamentally misaligned with the requirements of tokenised finance products. Legacy core banking systems are typically structured around specific product verticals, each difficult to modify; legacy payment systems are similarly fragmented, built around specific rails with limited flexibility to adapt. These platforms were not designed to coordinate across distributed ledger networks or to orchestrate transactions spanning traditional and tokenised systems. Extending these legacy systems to support this new paradigm requires expensive architectural changes that the software - and the organisation - will structurally resist.

The sidecar coexistence approach as a stepping stone

Some banks deploy a “sidecar” core to ledger tokenised finance products alongside their existing infrastructure. This can be an effective approach for rapid proof-of-concepts. But scaling these initial experiments requires more than just a new ledger. Banks require payment orchestration capabilities to coordinate operations across the sidecar, legacy systems, and external networks. This means managing transaction atomicity, failure recovery, and state synchronisation across platforms that were not designed to work together. Choosing the right sidecar platform becomes critical. Banks that select platforms with modern, highly configurable, and performant payment orchestration built in can launch new tokenised products and scale them through configuration updates. Those that deploy ledger-only solutions must build additional payment infrastructure or wait for vendor customisations.

Financial institutions should treat the sidecar as a stepping stone, not the destination. When evaluating sidecar platforms, consider the target state of unified infrastructure capable of operating across both traditional and tokenised finance. The right platform offers the flexibility to evolve from experimental sidecar to a strategic foundation, avoiding the technical fragmentation that permanent parallel systems create.

The Vault Platform: the strategic platform for traditional and tokenised finance

The Vault Platform is a unified system that integrates core banking, payments, and operations in a single architecture, designed to operate across both traditional and tokenised financial systems.

The platform can integrate with a curated network of partners operating in the tokenised finance ecosystem. This enables banks to launch tokenised products rapidly without lengthy vendor evaluation, legal negotiation, and technical integration. In addition, the platform maintains vendor neutrality, giving banks flexibility to work with their preferred partners in the ecosystem or their in-house services.

At the heart of the platform are a highly composable ledger, Vault Core, and a universal payments engine, Vault Payments. Banks can model any financial product they envision, from traditional retail banking products to tokenised asset-based lending. They can also configure payments that route across traditional payment rails, card networks, blockchain networks (public or private), Vault Core, legacy core banking systems, and other first and third-party services.

With Vault Platform, banks can launch hybrid products that were previously unviable with legacy architecture. Instant fiat loans secured by tokenised collateral, cross-border payments that seamlessly convert between fiat and stablecoins, debit cards backed by stablecoin balances - these are just the beginning. Banks can configure any products they envision using flexible building blocks available through the platform from day one.

Finally, the platform provides a unified operational interface for the bank. Payment operations teams can monitor and resolve exceptions from a single interface across all rails. Risk and compliance teams can generate consolidated reports across traditional and tokenised exposures. Product teams can configure new offerings through composable building blocks without engineering dependencies. With Vault Platform, each function in the bank gains the visibility and control required to operate in this hybrid environment.

Experiment fast with a strategic end in mind

For financial institutions, the window to establish positions in tokenised finance is open now. Those who begin experimenting will develop an understanding of the operational realities, technical requirements, and customer opportunities. They can identify the propositions that deliver genuine value for their customers and establish an advantageous position before the competitive landscape hardens.

Thought Machine partners with financial institutions to navigate the emerging tokenised financial system. We work with banks to design and run proof-of-concepts that test real operational capabilities, and provide rapid learning without requiring wholesale transformation. These experiments create the foundation for informed strategic decisions about how to compete across both traditional and tokenised systems.

The Vault Platform serves as strategic infrastructure for the long term. Banks that begin with proof-of-concepts on Vault Platform build on the same architecture they will use at scale. They can experiment efficiently whilst building towards a coherent long-term architecture.

The reshuffling in financial services is here to stay. For financial institutions, the time to engage with tokenised finance is now, with the best possible infrastructure and the right partner. Contact Thought Machine to learn more about how we can support your institution's journey into tokenised finance.

Head office:

7 Herbrand Street

London, WC1N 1EX

United Kingdom

Press email:

press@thoughtmachine.net